At its root, the solution is a change in mindset.

The whole point of having an economy is to support and improve the lives of the citizens, the people, who make up society. The economy isn't a goal in itself. Benefiting "the economy" has no value if it doesn't benefit actual people. There is no principal involved - any principle which does not actually make life better for real life people is necessarily an invalid principle.

There is a widespread misunderstanding of the Amish approach to technology. The Amish are not luddites. They simply question the value of each and every use of technology on an individual case by case. So while they may not find that the use of tractors in general improves life for their society, if a particular farmer is disabled, he might be granted an exception.

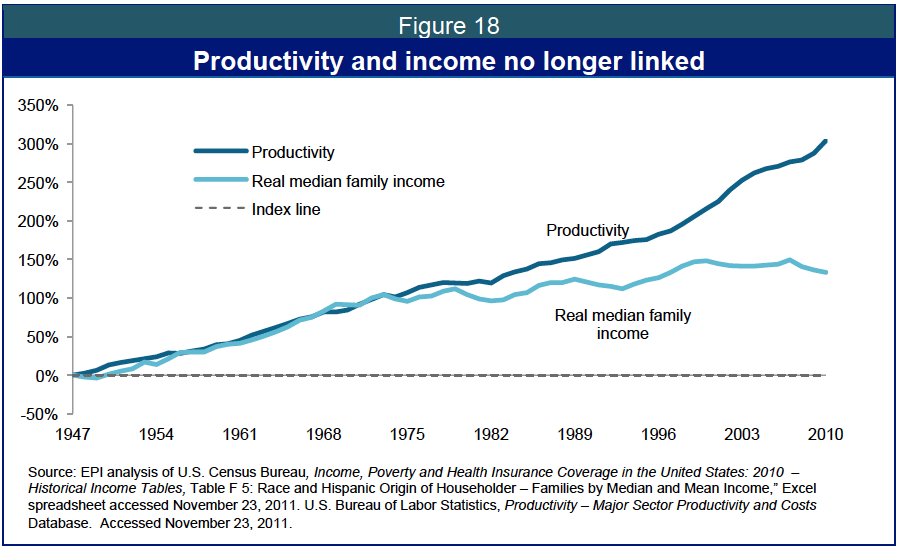

If the entire point of the economy is to benefit society as a whole, it makes sense to question whether or not that end goal is being accomplished. As the graphs in part 3 show, it is not. Maximizing growth had value when the nation was young and growing, but today we are grown, and conditions have changed.

Our current system gives the biggest reward to people who do no actual productive work, thereby decreasing the pool of wealth and resources available to everyone else. It keeps employment up only by constantly growing, ensuring rapid environmental destruction and unnecessarily stressful lives for everyone but the upper 0.01%, with some people working 40-50 hours a week and others working none at all.

This would all be easy to fix - and far from socialistic idealism, doing so would require less government intervention, and more free markets.

The trick is to remove all those government creations whose sole purpose is supporting capitalism.

Stop issuing deeds for investment property. Everyone should be able to have the opportunity to own the land on which they live - having a place to exist is as much a fundamental human need as water and air. And, like water and air, we can choose to place limits on what an individual can claim ownership over. No one can buy a river, and no one can claim title to a chunk of atmosphere. If government refused to issue titles, and refused to enforce claims of ownership of property which the owner was not personally using, there would be no such thing as investment property. Each individual could own exactly 2 parcels of land - one on which they live, and one for a business.

Stop issuing corporate charters- or at least look at them on an individual case-by-case basis, as the Amish would, and approve them if - and ONLY if - it is determined to be in the best interest of society as a whole.

Instead of issuing a corporate charter of indefinite length to anyone who applied, a charter could be (as they originally were) for a fixed period of time - say 1 year. After a year, the corporation is dissolved. For any time longer than that, the applicants would have to demonstrate that its existence would not just profit the shareholders, but would provide some tangible benefit to society that could not be provided any other way, and which more than compensates for it's inherently anti-competitive, anti-free-market nature.

Never allow any corporations to merge, and severely limit the ability of privately held companies to buy each other - this last is a government regulation, but it is one that preserves the integrity of competition, which is a prerequisite for free markets to operate efficiently.

Tie working hours to productivity. If, for example, the invention of computers increases the overall average productivity per worker by 100%, then overtime law should be adjusted to begin paying time and a half at 20 hours per week. Again, this preserves an existing regulation, but it is necessary to offset the effect that technology has on income inequality and the labor market (and it isn't a new regulation, but merely an adjustment to an existing one - does anyone really want to go back to before there was such a thing as a "weekend"?)

Instead of copyright lasting for an entire lifetime after the author dies, it could be based on compensation - once the creator has sold enough to make back their investment plus living expenses, maybe a nominal percentage profit on top (10%? maybe even be generous, and say 25%), once that threshold has been reached, the copyright would automatically expire, and it would enter the public domain.

In the age of the internet, an investment in technology or software or media can become profitable within months, sometimes days, of going public. There is no reason to leave technology to profit a single individual for 20 years - the moment the investment pays off, there is incentive to have made the investment.

Stop underwriting the finance industry. Not just the occasional bailout, but ongoing stuff like free insurance and below market rate loans, give banks and investment firms a huge advantage using tax payer dollars.

Tax unearned income at a rate at least as high as earned income - in our current system, money you get just because you already have money - snowball money - is actually taxed less than money you earn by going to a job, working hard, and producing something of tangible value to society. Although it is not the biggest reason for income inequality, it is certainly one of the most blatant ways we have set up rules to benefit the already rich at the expense of everyone else.

All these steps would serve to level the playing field, so to speak. If the playing field is level, then snowballs can't take off under their own weight. No one would be limited from getting rich - people could make their snowballs as large as they want - but a person would have to roll it themselves. We would have a true merit based society, where the rich earned not just their seed money, but every penny along the way, by producing value and contributing to society.

Economic growth would slow, but that would be ok, because we have enough already.

With all the excess wealth no longer going to the investment class, there would be plenty left over to raise per hour wages, which would allow everyone to make a decent living with far fewer working hours, which would more than compensate for jobs lost due to less economic growth. If working hours were reduced proportionately to how much productivity has increased since the 40 hour week was instituted...

...the standard work week would be 5 hours, increasing job openings by 800% - there would be no unemployment, and the market would naturally drive up wages as employers competed for employees.

Instead of some working overtime (plus long commutes and mandatory lunch breaks), some collecting government checks, and others living on investments, everyone who could work would work, but no one would have to work more than an hour a day.

This vision is so far from today's reality that it seems idealistic, utopian, downright silly. But the numbers work. It only seems unrealistic because it is so hard to conceptualize just how enormously much wealth the upper 0.1% skims off the top of the productivity of everyone else.

Eighty-five people control the same amount of wealth as half the world's population.

That is 85 people compared with 3.5 billion. That's all snowball money. All those resources being so concentrated is the reason everyone else has to work 40 hours a week, despite all the gains that technology have brought to production.

|

| (What a funny coincidence, this looks just like those last graphs!) |

This didn't "just happen". It isn't the inevitable consequence of the free market. It began when government started instituting laws and policies which were, in theory, pro "business" and growth, but in reality which much more specifically pro "large corporation", at the expense of small independent business. The citizenry has gone along with it, seduced by the claim that what is good for giant corporations is good for America as a whole. Because the effects are gradual, and diffuse in a very complex system, most never noticed the consequences as they happened - and those who did usually jump to a reactionary opposite extreme such as anarchy or communism, and as a result get written off altogether.

If we recognize that the free market and capitalism are not the same thing, that capitalism is better for growth but the free market is better for equality of opportunity, average standard of living, the environment, and the well being of everyone (even those who would only be wealthy instead of rich, since additional money has zero marginal utility to the already wealthy, but they would live in a world with more stability and less crime) - then the solutions to the problems of capitalism are obvious.

The only question left is, how do we go about actually instituting them?

[UPDATE: A friend who read this asked me for any ideas on how, as an individual, we might work towards a free market future. This is what I came up with: http://biodieselhauling.blogspot.com/2014/06/walk-talk.html ]